How wealthy Chinese move hundreds of billions abroad to buy assets

Capital flight remains a concern for the authorities. But experts think the government has it under control, for now

PUBLISHED : Tuesday, 09 August, 2016

Since China abruptly depreciated its currency last August, the country’s wealthy have been trying to bypass the strict capital controls and transfer money abroad in many inventive ways, in search of better-yield investments.

But analysts say the capital flight could stabilise, if the central bank effectively increases two-way flexibility of the exchange rate and tames the expectations of a falling yuan.

As of Monday, the yuan’s official mid-point rate against the US dollar had plunged 9 per cent since August 11, 2015, when the People’s Bank of China stunned markets by lowering the daily fixing by 1.9 per cent, the largest cut ever.

The yuan has also slumped against most of its major currency rivals, down more than 10 per cent and 30 per cent respectively against the euro and the yen in the past 12 months.

Expectations of a declining yuan, combined with the gloomy economic outlook, have sparked unprecedented capital outflows.

The most recent data shows China’s FX reserves declined by US$4.1 billion in July to US$3,201 billion. Compared with the end of July in 2015, the reserves have shrank by US$450 billion.

“Although the capital outflow pressure has eased from 12 months ago, it still persists,” said Larry Hu, an analyst for Macquarie Research.

“A considerable portion of the outflows may be due to Chinese residents’ buying overseas assets, as they seek better and safer investments amid the decline of the home currency,” he added.

China does not publish detailed figures about its capital outflows. But according to an estimation by Goldman Sachs in July, there were US$372 billion in outflows by Chinese residents spent on foreign assets in the second half of last year, and another US$108 billion left the country in the first quarter.

Separately, net capital outflows amounted to US$123 billion in the first quarter, compared with US$504 billion in the second half of last year.

“In Q1 this year, ... and in H2 last year,... residents buying foreign assets accounted for around 70 per cent of the outflows,” they added.

The official methods of Chinese residents’ accumulation of FX assets include outward direct investment, portfolio investment assets, and other investment assets, according to the headline reported data from SAFE.

However, Goldman analysts add the negative numbers in “net errors and omissions” might also represent disguised capital outflows, as that number ballooned in the third quarter of last year (See below chart).

However, Goldman analysts add the negative numbers in “net errors and omissions” might also represent disguised capital outflows, as that number ballooned in the third quarter of last year (See below chart).

China imposes strict capital control on residents, only allowing each individual to buy no more than US$50,000 in overseas assets annually.

Nonetheless, “there are some policy loopholes which people use to disguise their capital flight,” Hu from Macquarie said.

“A widely used method is to fake invoices, such as overstating the value of imports,” he said.

For example, a Chinese company imports a machine and invoices it at US$1 million, while it’s actually worth US$500,000. The company pays the actual amount and puts the rest of the money in offshore bank accounts or invests it in other overseas assets.

Although the Chinese banking regulator has tightened the scrutiny of residents’ overseas transactions, “ it’s hard to eliminate those activities, ” Hu said.

And Hong Kong is being used to disguise such capital outflows, experts say.

“Much of that money feeds through Hong Kong,” said Victor Shih, a professor at University of California, San Diego.

Although the capital outflow pressure has eased from 12 months ago, it still persists

Imports from Hong Kong have surged since December, official statistics from China show.

In July, imports from Hong Kong grew 143 per cent year-on-year. In June and May each, imports from Hong Kong soared 144 per cent and 243 per cent.

Chinese customs officials had previously attributed much of the surge to China’s increasing imports of gold from Hong Kong.

However, analysts say the figures still look a little suspicious.

“Growth momentum like this looks very unusual, given the overall grim picture of imports and exports, though the base was comparatively small in 2015,” said Andrew Collier, managing director of Orient Capital Research.

He said he’s been told by industry insiders that the number was likely inflated by bogus transactions that served as capital flight, a common practise among importers.

“In addition, more than half of imported goods from Hong Kong are jewellery, precious metals and related products. These low-weight but high-value commodities are ideal for virtual-high price quotations,” he said.

Other methods of disguising capital flows include overstating the amount of an overseas M&A, Collier added.

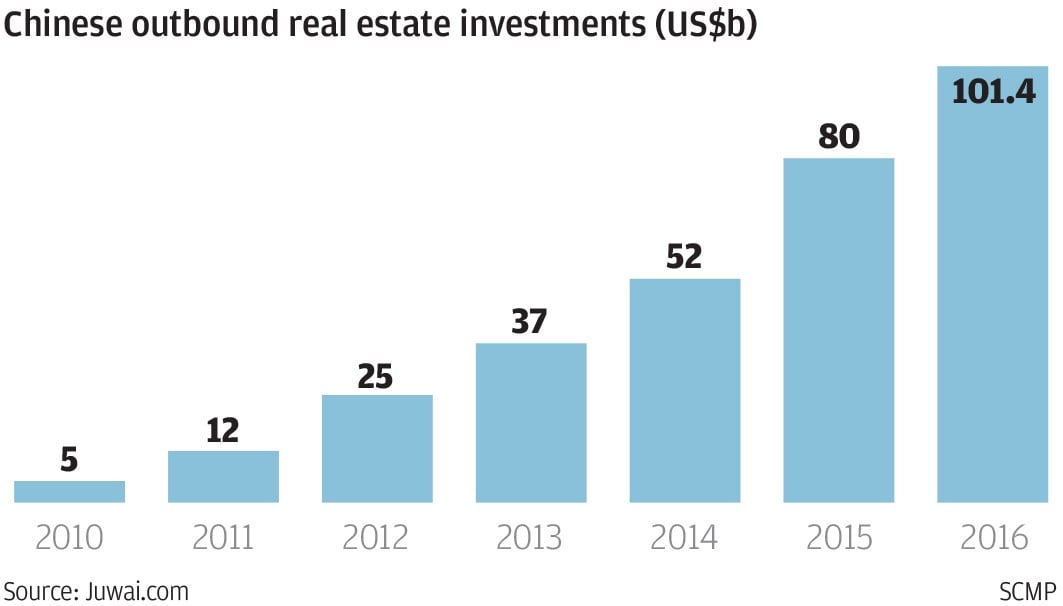

“Chinese enterprises made outward direct investments totaling US$118 billion across all industries in 2015, up by 14.7 per cent from the previous year,” he said.

“However, much lower-than-expectation profitability of these overseas projects is what truly defines the nature of China’s ODI largely as capital flight.”

But for individuals who want to sneak out more than US$50,000 to buy overseas assets, such as a house in New York or Vancouver or Sydney, a popular way is to pool quotas of a group of family members or friends, with each person transferring US$50,000 out of the country.

The process is called “smurfing” in the banking industry, or “ants moving their house” in Chinese.

Another widely known method by individuals is to use underground private banks, which are popular in China’s southeastern provinces such as Guangdong.

A Chinese resident can deposit 1 million yuan in his account in a domestic private bank, and take out the same value of money in foreign currencies, such as Hong Kong dollar or US dollar, in the overseas branches of the bank as quickly as within hours.

Regardless of the methods being employed, however, Hu from Macquarie Research says the underground outflow to Hong Kong is still “manageable” for Chinese regulators, as total imports from Hong Kong are relatively small compared with overall imports.

He also expects the capital flight to moderate, as the yuan has stabilised in recent months and the market has also reacted more calmly to the currency’s depreciation.

“If the PBOC can introduce more two-way flexibility of the exchange rate and effectively manage market expectations, residents will probably reduce their bets on the yuan’s decline,” Hu added.

He expects the yuan to reach between 6.6 to 6.8 against the US dollar by year-end, albeit “with more fluctuations”.

No comments:

Post a Comment

Comments always welcome!