Beyond Huawei, Scientist’s Death Hurts China’s Technology Quest

The loss of renowned physicist Zhang Shoucheng highlights tensions over Chinese venture capital investments in U.S. technology startups.

The death of a prominent Chinese scientist in the U.S. has passed comparatively unnoticed beside the blizzard of global headlines devoted to the Huawei dispute, yet the tragedy bears upon another important aspect of Beijing’s quest for technological leadership.

Zhang Shoucheng, an internationally recognized Stanford University physicist and venture capitalist, died on Dec. 1, the same day that the chief financial officer of Huawei Technologies Co. was arrested in Vancouver. The 55-year-old had been battling depression, the South China Morning Post reported, citing an email from the Shanghai-born scientist’s family. In a later statement, the family said there was no truth in speculation on Chinese social media that Zhang’s death was connected to a possible U.S. government investigation into his venture capital fund, the newspaper reported. The scientist, who had been tipped as a future Nobel Prize winner for his work on quantum physics, founded a $400 million fund that invests in Silicon Valley startups and was active in helping U.S.-trained Chinese researchers to return home.

Zhang Shoucheng, an internationally recognized Stanford University physicist and venture capitalist, died on Dec. 1, the same day that the chief financial officer of Huawei Technologies Co. was arrested in Vancouver. The 55-year-old had been battling depression, the South China Morning Post reported, citing an email from the Shanghai-born scientist’s family. In a later statement, the family said there was no truth in speculation on Chinese social media that Zhang’s death was connected to a possible U.S. government investigation into his venture capital fund, the newspaper reported. The scientist, who had been tipped as a future Nobel Prize winner for his work on quantum physics, founded a $400 million fund that invests in Silicon Valley startups and was active in helping U.S.-trained Chinese researchers to return home.

His death highlights a deep pool of Beijing-backed money that has been passing under the public radar.

Consider the fund Zhang founded. Danhua Capital was cited in a report last month by the Office of the United States Trade Representative after an investigation into China’s technology policies and practices.

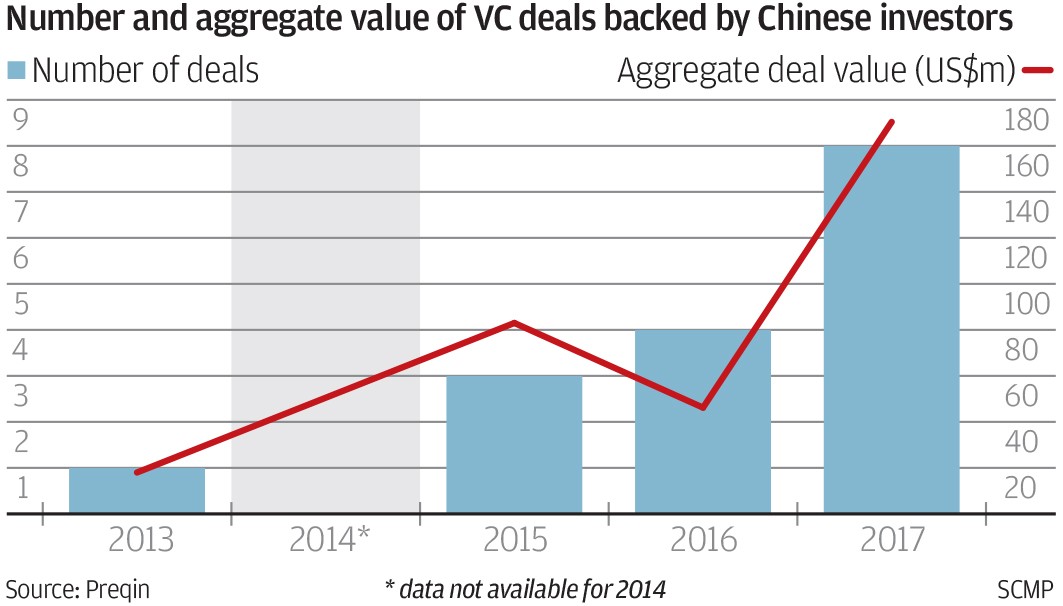

The way the USTR sees it, China is infiltrating Silicon Valley. Between 2015 and 2017, 10 percent to 16 percent of venture capital deals counted Chinese investors as participants.

Infiltrators

Chinese investors are increasingly active in the U.S. venture capital world

The report singled out Zhang’s firm as an example of the new tactics China is using to obtain U.S. technology. The fund lists 113 U.S. companies in its portfolio, most falling within emerging sectors that the Chinese government has identified as strategic priorities, according to the report. At least one “has reportedly decided to reduce operations in Silicon Valley and open operations in China,” it said.

For years, China relied on government subsidies to encourage development of key industries. But starting in 2014, subsidies gave way to so-called “guidance funds”, or state-backed funds of funds that act like venture capital and private equity firms. As of the first half, various levels of the government had established 1,171 guidance funds, aiming to raise and deploy a staggering 5.9 trillion yuan ($858 billion).

Venture Capital, the China Way

State-backed guidance funds have exploded since 2014. Here are some of the largest

Danhua Capital, also known as Digital Horizon Capital, is a major beneficiary of China’s shift into guidance funds. It counts Zhongguancun Development Group, a state-backed investment fund with more than 10 billion yuan in assets, as a major investor. The firm invests in artificial intelligence, big data, blockchain and other disruptive technology sectors.

To be sure, there is no evidence that Danhua Capital has been following Beijing’s bidding. And government-backed venture capital funds aren’t a Chinese invention. Beijing may have been inspired by the U.S., where the Small Business Innovation Research program made early investments in Apple Inc. and Intel Corp. The U.S. Small Business Investment Co. has $26 billion in assets under management.

But one can see why these Chinese state-backed funds make the U.S. government nervous.

The scale is unprecedented. For instance, the $21 billion China Integrated Circuit Industry Investment Fund, established in September 2014 and nicknamed the “Big Fund,” is reportedly raising another $47 billion this year. In addition, there’s already evidence that shows China is abandoning fund-of-funds best practices.

In a 2014 interview, Zhongguancun, set up in the early 2000s long before the recent explosion of guidance funds, said that it would contribute to no more than 30 percent of the total capital of venture capital funds in which it invested, and that it would not interfere with fund managers’ decisions. In other words, it would act only as a passive investor.

But the new kids on the block aren’t abiding by the old rules. For instance, this May, China’s largest chip foundry company, Semiconductor Manufacturing International Corp., partnered with the Big Fund to establish a new 1.8 billion yuan venture capital vehicle. The fund is clearly in the driver’s seat: It contributed 49.5 percent of the capital and owns 15 percent of SMIC.

In August, the U.S. government signed an update to legislation for the Committee on Foreign Investment in the U.S., broadening governmental scrutiny to vetting VC-backed, and especially Chinese state-funded, investments in U.S. tech startups.

With Zhang’s death, China has lost a valuable connection to the newest technology in Silicon Valley. But my bet is that Beijing won’t ease back on its aggressive tactics. The wall of money is too big and the strategic imperative to upgrade China’s technology is too great.

No comments:

Post a Comment

Comments always welcome!