"Fake Chinese income" mortgages fuel Toronto Real Estate Bubble: HSBC Bank Leaks

“I found out a huge mortgage fraud showing borrowers with exaggerated income from one specific country, China": The Bureau investigates whistleblower docs

The whistleblower, a Canadian business school graduate, was staggered by the suspicious home loans he discovered in 2022 when he joined a mortgage approval team in a small HSBC branch on the outskirts of Toronto.

He knew of suspicions surrounding Chinese capital in British Columbia real estate, but had never witnessed shady lending while working at an HSBC branch in Campbell River, a bucolic town on the coast of Vancouver Island.

When he arrived at HSBC’s bank in Aurora, an affluent suburb north of Toronto, he discovered explosive growth in home loans to Chinese diaspora buyers during the Covid-19 pandemic.

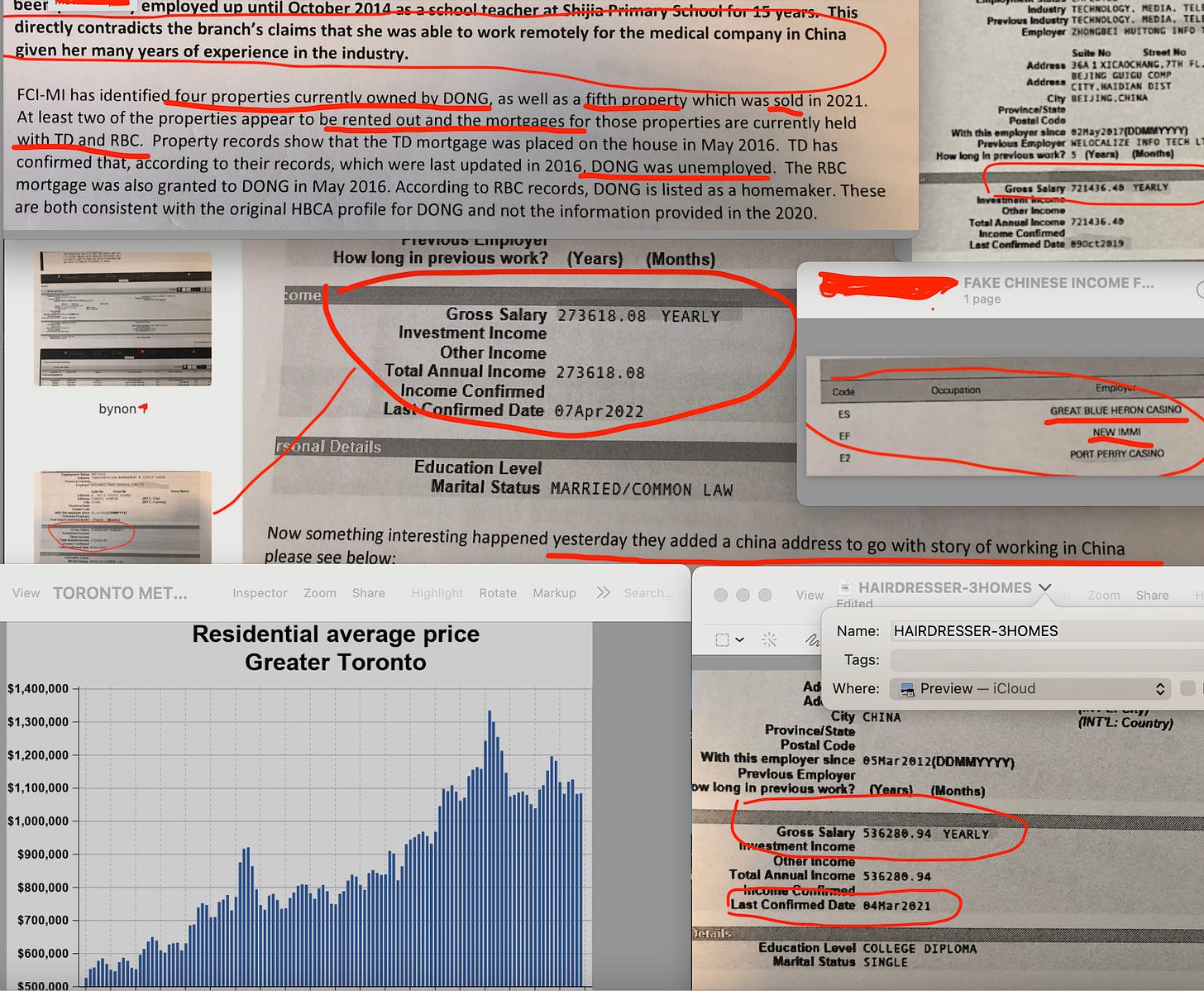

Chinese migrants living across Toronto were obtaining mortgages from HSBC while supposedly earning extravagant salaries from remote-work jobs in China. In one example, an Ontario casino worker that owned three homes also claimed to earn $345,000 in 2020 analyzing data remotely for a Beijing company.

Before joining HSBC Canada, the whistleblower had studied fake-income mortgage frauds for his Business Masters degree at Vancouver Island University. After arriving at Aurora in February 2022, while digging into the branch’s loan books and interrogating his colleagues, he discovered mind-blowing assessments.

Since 2015, the whistleblower concluded, more than 10 Toronto-area HSBC branches had issued at least $500-million in home loans to diaspora buyers claiming exaggerated incomes or non-existent jobs in China.

These foreign-income scams spiked during the pandemic, the whistleblower believed, because borrowers could somewhat plausibly claim to be working remotely in other countries while riding out Covid-19 in Canada.

While a small bank of Aurora’s size was expected to issue about $23-million in residential loans every year, this branch had shovelled out $88-million in mortgages in 2020, according to the whistleblower, and over $50-million in 2021.

The whistleblower, whom The Bureau is calling D.M., emigrated to Canada as an international student from India, making him a minority among mostly Chinese-Canadian co-workers at the Aurora branch.

As D.M. probed his colleagues, his belief gained conviction, that HSBC Canada and other Canadian banks including CIBC had systemic problems with highly questionable mortgages issued to diaspora buyers with unverified sources of wealth in China.

Losing sleep, in April 2022, D.M. sent an audacious email to senior bank executives: “I am going to reveal potential mortgage fraud at HSBC Bank Canada and possibly some employees benefited from the fraud, financially pocketing thousands of dollars, which I call the proceeds of crime.”

D.M.’s explosive four-page complaint triggered an internal investigation that led to some reforms at HSBC Canada according to internal emails obtained by The Bureau.

But more than a year later, D.M. was so dissatisfied with the bank’s response that he risked sharing his story and numerous internal documents for an unprecedented journalistic investigation into Canada’s housing affordability crisis.

“I found out a huge mortgage fraud showing borrowers with exaggerated income from one specific country, China, pretending to be working remotely,” D.M. informed The Bureau in June 2023. “I believe the housing prices in Toronto are linked to this, because this is about income verification in banks, which is supposed to moderate demand.”

The Bureau asked HSBC Canada to review emailed information for this story and provide an appropriate manager for an interview regarding D.M. 's records and allegations.

“I won’t have anyone to speak with you directly,” Sharon Wilks, Head of Communications, responded. “But for context: As a global bank, HSBC is at the forefront of efforts to identify, prevent and deter financial crime … We will not do business with individuals or entities we believe are engaged in illicit conduct.”

Wilks added that HSBC Canada “can and do regularly exit relationships with clients whose activities we deem too risky.”

The Bureau’s seven-month investigation into D.M.’s allegations suggests HSBC Canada and other Canadian banks could have issued many billions of dollars in questionable mortgages to Chinese diaspora buyers, and a significant cause of Canada’s real estate bubble is hundreds of billions in illicit fund transfers from China into Canada, and bank lending that amplifies its impacts, especially in Toronto and Vancouver home prices.

“There are thousands of these cases, large scale,” D.M. said in an interview. “Hardworking Canadians are denied mortgages and these Chinese residents forge documents and get mortgages approved, heating up the already hot Ontario real estate markets.”

“These people don’t have steady jobs or income in Canada,” he said, “but what they are doing is scams to launder money, and get mortgages using fake documents.”

The Bureau’s investigation included asking seven prominent Canadian experts to assess some of D.M.’s documents, allegations and conclusions.

This investigation suggests D.M. 's calculation is plausible, that the Aurora branch and other Toronto-area HSBC branches have issued at least $500-million in questionable Chinese income loans since 2015.

But D.M’s findings could also change the public’s understanding of housing affordability in Toronto and Vancouver, a politically explosive issue expected to frame Canada’s upcoming federal election.

This is because, according to the academics and criminologists that reviewed D.M.’s documents with The Bureau, his evidence fits into FINTRAC’s much broader examinations of suspicious real estate and banking transactions.

In 2023, the anti-money laundering watchdog published a ground-breaking study into 48,000 Chinese diaspora banking transactions.

FINTRAC found that during the Covid-19 pandemic, because Canadian casinos were closed, Chinese underground banking schemes evolved, flooding electronic fund transfers from Hong Kong into Canadian bank accounts that served like corridors for murky real estate transactions.

The Bureau’s analysis also finds that what D.M. discovered in Toronto banks, finally sheds light on mysterious capital flows discovered by a prominent Canadian academic in 2015, in a study of Vancouver land titles and mortgages.

That examination of $525-million worth of real estate purchases in a six-month period found 66 percent of buyers in several affluent neighbourhoods were recent Chinese diaspora migrants, and most mortgages went to buyers with little or no income in Canada.

Similarly, what D.M. found in his probe of pandemic-era loans could be called the evolving “Toronto Method” of an underground banking system discovered first in Vancouver, and found to be laundering a stunning $1.2-billion in cash from Mainland China through British Columbia government casinos in 2014.

This system of shadowy transfers was dubbed the “Vancouver Model” by an Australian professor, and brings together transnational organized crime, affluent Chinese nationals seeking to export their wealth abroad, and Canadian casinos, banks and real estate, in transactions that evade policing because the pivotal cash exchanges are done off the books by professional money launderers serving the global Chinese diaspora.

According to FINTRAC’s 2023 study of 48,000 pandemic-era transactions, this evolving Vancouver Model network “simultaneously facilitates money laundering and the circumvention of Chinese currency controls”

“As a result of the temporary closures of Canadian casinos due to the COVID-19 pandemic, professional money launderers began to diversify their money laundering methods,” FINTRAC’s study says.

“During this time, FINTRAC observed a rise in money laundering typologies involving transferring large sums of funds to Canada from foreign money services businesses, often located in China, notably Hong Kong, and the laundering of the funds primarily through the real estate, securities, automotive and legal professions.”

These wire transfers from China were routed into bank accounts of “multiple, unrelated individuals in Canada,” that served as “money mules” in byzantine networks involving Canada-based real estate developers, real estate agents, mortgage brokers and banks.

These Chinese diaspora bank account owners often claimed they were students, homemakers, office managers, or unemployed, FINTRAC reported.

They sometimes used their accounts to send bank drafts to others in Canada for home purchases, or served as “straw buyers” for offshore investors.

“Mortgage payments are sourced from incoming funds from China,” FINTRAC’s alert said.

FINTRAC’s study doesn’t say that Canadian banks knowingly issued fake-income mortgages to Chinese diaspora buyers in Toronto.

But in an interview, D.M. said banking staff are trained to guard against fraud, and the loan application packages he reviewed in Aurora beggared belief.

“The bank found out that one lady works in a casino part-time but got a $1.4 million mortgage showing over $300,000 annual income,” he said. “Plus she takes money as benefits from the government, for her two kids.”

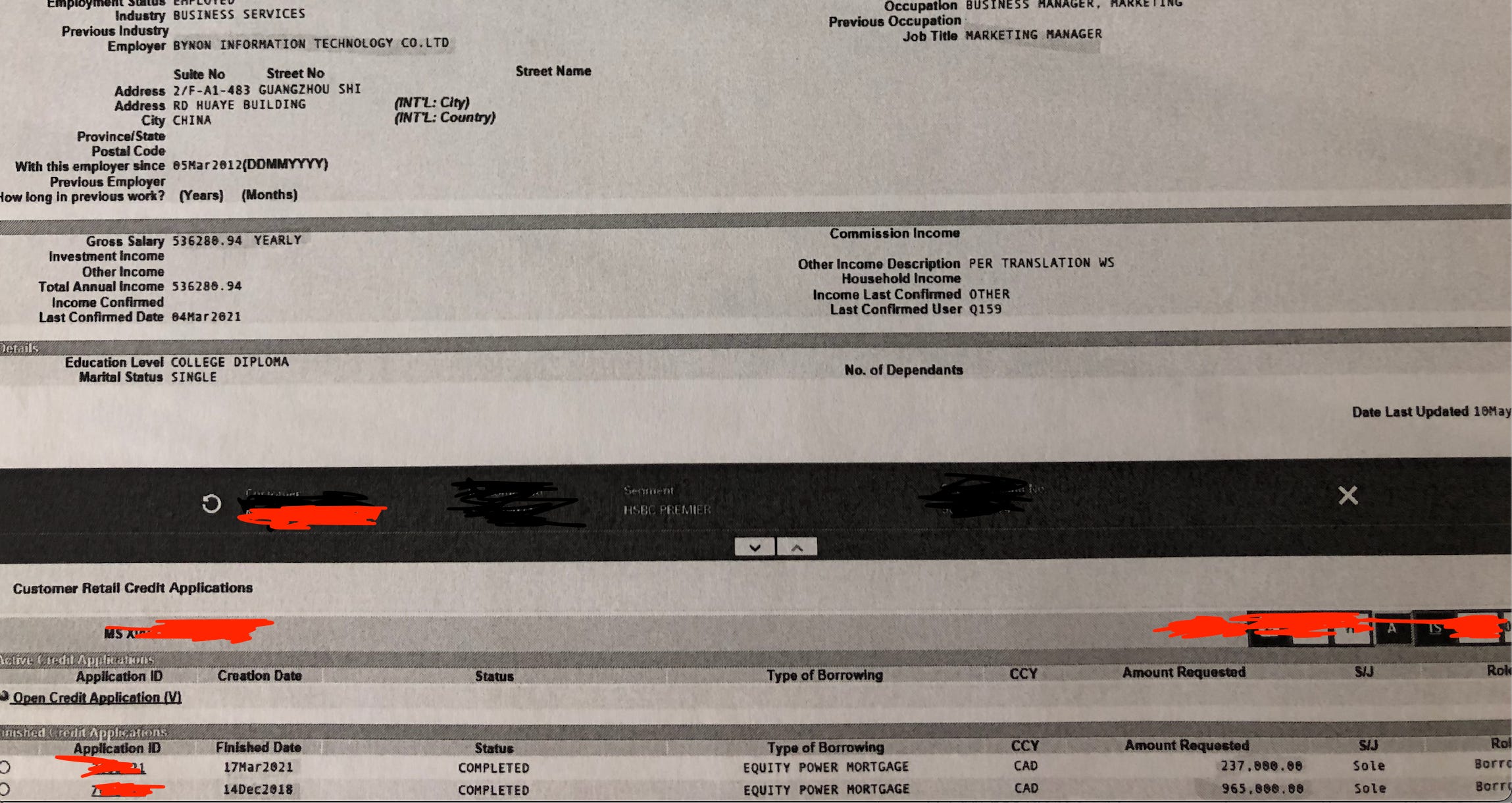

In other examples, an HSBC mortgage client claimed to earn $700,000 annually for remote work in China, while simultaneously living in Canada and paying off a $10,000 student loan.

Another woman who owned homes in Aurora, Markham and Scarborough, worked part-time as a hairdresser while also claiming to earn $536,280 at a “Business Manager” job in Guangzhou.

“Canadian workers have been put out of the real estate market by people working as a hairdresser that own a couple homes,” D.M. said in an interview.

“How is that fair?”

The most shocking case reviewed by The Bureau, shows that one woman that owns at least four Toronto properties opened her HSBC Aurora bank account in 2013, claiming to be a “Homemaker with no annual income.”

But her Toronto account soon received incredible amounts of wire transfers from HSBC China accounts, and paid out “high value cheques” to third parties for real estate purchases.

This case suggests “Toronto Method” shadow banking described in FINTRAC’s 2023 study has been seeping into Toronto real estate for about a decade.

And yet in 2020, this same woman applied for another HSBC Canada mortgage, claiming to earn $763,000 remotely from her job in China.

This evidence from the HSBC whistleblower complements the seminal investigations of Simon Fraser University academic Andy Yan, who examined sales from August 2014 to February 2015 in several communities on Vancouver’s westside. The average home price in Yan’s study was $3-million.

Looking back at his Vancouver findings in comparison to D.M.’s Toronto banking documents, Yan told The Bureau “I think this helps affirm some of my early work that I did, almost nine years ago.”

“This goes to the core of our banking system,” he said, “and how are we verifying identities and how are we verifying incomes.”

In Yan’s controversial study the vast majority of mortgages went to buyers listing their occupation as home-maker, followed by students, and managers. HSBC and CIBC were the dominant lenders.

Unlike the HSBC whistleblower, Yan had no access to internal banking data regarding the purported origin of funds behind these mortgages taken by Chinese diaspora buyers.

But in an interview, Yan said what he found most interesting back in 2015, was suspicions that Chinese migrants were often buying homes with bulk cash, weren’t accurate. The truth was more complex and seems to be clarified by D.M.’s mortgage findings in Toronto.

“It's about that global flow of capital, and how it's multiplied by Canada’s mortgage and lending system,” Yan said. “Because you have to remember, one of the biggest conclusions about my study was that it wasn't bags of cash that were being used to purchase Vancouver homes outright. They were loans being used. So now, I’m thinking, this is where my study connects up to what you have discovered in Toronto.”

“The interesting story here,” Yan added, “is what happens in Toronto real estate may not repeat Vancouver, but it perhaps rhymes.”

Probably the most famous Chinese property owner from Yan’s 2015 study areas is Huawei executive Meng Wanzhou. In 2009 her family bought a home in Vancouver’s Dunbar neighborhood for $2.73 million, land titles show. In 1998, ten years before Vancouver Model transactions started to surge in Vancouver real estate, the home was sold for $370,000. The home is now valued at almost $6-million.

Ashleigh Rhea Gonzales, a former RCMP data scientist who recently published a criminology thesis finding Chinese diaspora underground banking causes significantly more money laundering into Canada’s real estate than previously estimated, said that D.M.’s findings resemble her own Vancouver Model research.

“This whistleblower’s allegations of widespread mortgage fraud at HSBC Canada align with some of the first-hand accounts from staff of some Canadian financial institutions that I have come across in my research on money laundering in British Columbia,” Gonzales said.

Gonzales, who worked for RCMP’s anti-gang unit in British Columbia until 2023, says she found reports of mortgage fraud accelerated “during the uptick in the Canadian housing bubble after the Vancouver 2010 Olympics,” and continued to surge from 2015 to 2018.

With all this considered, and comparing data sources in this story with previous evidence confirmed in British Columbia’s Cullen Commission, The Bureau estimates that from 2014 to 2023, well over $200-Billion in Vancouver Model and Toronto Method funds could have poured through underground diaspora networks and Canadian financial institutions into Toronto and Vancouver’s real estate.

A federal official not authorized to comment publicly also examined D.M.’s banking leaks for The Bureau, and called this information “explosive.”

The official said money laundering is increasing in Canada, and D.M.’s belief that Chinese-income mortgage fraud has boosted home prices in Toronto is true, but also should apply for Vancouver and Montreal real estate prices. The official noted that other nations require tax agencies to verify incomes for mortgages, which isn’t the case in Canada.

“It matters for our next generation because of the impact on the housing market,” the official said.

Queen’s University professor Christian Leuprecht – editor of Dirty Money, a new academic text that probes how Ottawa’s weak regulation has “turned the Canadian federation into a destination of choice for global financial crime” – also reviewed some of D.M. 's leaks.

“It’s not a new problem, but you’re taking it to the next level,” Leuprecht said.

“Why does this matter? Because organized crime isn’t just laundering their ill-gotten gains, like any good business person, when they buy real estate, they generate a down payment, then get a mortgage for the rest. Why buy one property when you can buy four?”

“Do you know how many mortgage frauds we have in our books?”

The Bureau’s review of HSBC Canada emails and D.M.’s text messages, shows he came to believe numerous employees at the Aurora branch had direct knowledge of faked Chinese income mortgages, and a veteran manager with oversight of more than 10 Greater Toronto branches knew about broad and questionable mortgage lending for Chinese diaspora clients.

Months after D.M. blew the whistle internally he exchanged texts with another employee, identifying colleagues that they believed had knowledge of diaspora mortgage scams.

The texts suggest D.M. believed HSBC Canada and other Canadian banks continued to hold vast amounts of suspicious foreign income mortgages, which could cause systemic loan quality risks if Toronto’s real estate prices decline.

“Do you know how many mortgage frauds we have in our books,” D.M. texted to his colleague. “It’s insane.”

“She told me,” the colleague replied, referring to an HSBC branch manager.

“She was like, if you do come, you gotta be prepared for the mortgage payout.”

“These people showed fake income and got mortgage,” D.M. continued. “Now interest rate is high, they can’t cope.”

“Other branches did the same thing too,” his co-worker replied. “I heard there’s a lot.”

“Absolutely,” D.M. texted. “All branches engaged in it.”

“This is like the unspoken secret,” his co-worker concluded. “I’m pretty sure other banks have it too. My Aunt have no income and got a mortgage for 700k. They just need a Covenanter from China.”

Toronto recently voted in Chinese/Canadian Olivia Chow as Mayor. Chow seeks more real estate and developers in her city, the claim being more affordable housing. This resonated in Trudeau's government and finance minister Freeland into supporting same, a distinct political move.

Questions arose about Chows financial backing during the election.

Two prominent community groups aligned with the Chinese government — including one that allegedly hosted a Chinese police station in Ontario — “went all out” to support Chow’s push to be mayor, supplying numerous volunteers to the effort, a letter from one of the groups claims.

A post on WeChat from Felicity Guo, deputy secretary general of the Canada Toronto Fuqing Business Association (CTFBA), one of the two groups, urged followers to back Chow. The message was accompanied by a photo of Guo, Chow and another woman.

The mayor-elect’s staff said that Chow never requested the two groups’ help, nor did they ask if she wanted it.

Vancouver also has their first Chinese Mayor, Ken Sim

No comments:

Post a Comment

Comments always welcome!